How to Pay for In-Home Care

When Sarah's 82-year-old mother needed daily assistance after a fall, her first question wasn't about care options. It was, "How much does 24/7 in-home care cost per month?" She was not alone in this concern.

When Sarah's 82-year-old mother needed daily assistance after a fall, her first question wasn't about care options. It was, "How much does 24/7 in-home care cost per month?" She was not alone in this concern.

Home care costs vary significantly based on location, level of care needed, and service hours. Understanding your payment options becomes essential for making quality care accessible at home, where comfort, familiarity, and independence matter most.

Whether you need immediate care solutions or are planning ahead, this comprehensive guide covers multiple funding options and strategic combinations that can help make home care affordable for your unique situation.

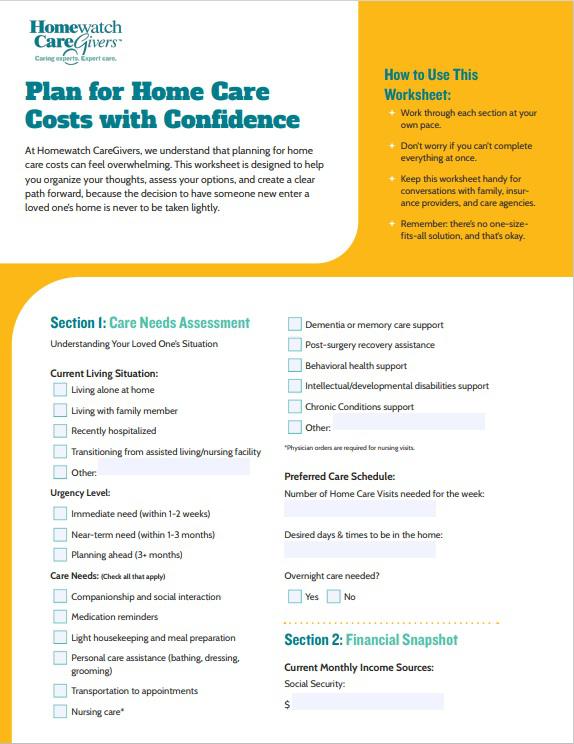

Use our downloadable Home Care Payment Planning Worksheet to compare these options and create a personalized funding strategy.

Table of contents (click to jump to each section):

- Section 1: Understanding Home Care Costs

- Section 2: Fourteen Home Care Funding Options

- Section 3: Creating Your Strategic Funding Plan

- Section 4: Working with Care Providers

- Section 5: Taking Action – Your Next Steps

- Section 6: Frequently Asked Questions about Paying for In-Home Care

Section 1: Understanding Home Care Costs

What Influences Your Home Health Care Cost?

The cost of in-home care for the elderly or other individuals isn't one-size-fits-all. Just as every person's care needs are unique, home care pricing varies based on several combined factors:

- Level of care needed (companion care vs. skilled nursing)

- Care Duration part-time vs. 24/7 in-home care)

- Geographic location and regional variations

- Provider qualifications and specialized expertise

- Special care requirements (dementia, post-surgical, chronic conditions)

Average Home Care Prices

Understanding these ranges helps you plan realistically while recognizing that quality care is an investment in maintaining independence and dignity at home.

- Companion care: $33 per hour nationally

- Personal care services: $34 per hour nationally

- Skilled nursing care: $350 per day nationally

- Overnight care: $720 per night nationally

- 24-hour care: $30 per hour nationally

Note: Home care rates and payment structures vary significantly by region and provider. Contact your local Homewatch CareGivers for specific pricing in your area.*

*Source: 2024 Genworth and CareScout Cost of Care Study, all figures are median.

Planning Your Home Care Budget: Real Examples

These examples show how different care levels translate into monthly investments, helping you understand what various levels of support actually cost.*

- Part-time support (20 hours/week): $2,720 per month*

- Full-time care (40 hours/week): $5440 per month

- Comprehensive care (24-hour in-home care): $21,823 per month

*Source: 2024 Genworth and CareScout Cost of Care Study, all figures are median.

Read more:

Section 2: Fourteen Home Care Funding Options

Most families don't rely on just one funding source. The key is understanding what's available and how different options can work together to create a comprehensive care funding strategy.

1. Medicare Traditional Coverage

Medicare home health care coverage provides specific benefits under certain conditions. While Medicare and home health care work together for skilled medical services, understanding exactly what's covered helps you plan effectively.

Medicare home care services include:

- Nurse visits for medical needs

- Physical therapy and occupational therapy

- Medical social services

- Durable medical equipment

How to qualify for home health care under Medicare:

- Must be homebound

- Need specialized medical services

- Services ordered by physician

- Use Medicare-certified agencies

How long will Medicare pay for home health care? Coverage continues as long as you meet medical necessity requirements and remain homebound.

While Medicare pays for home health care for medical needs, Medicare home care coverage doesn't typically include:

- Long-term personal care services

- In-home care for daily living assistance

- Companion care services

If you’re still unsure if Medicare will pay for home health care, read more about determining whether services are medically necessary versus personal care assistance:

- How to Qualify for Home Health Care Under Medicare: A Comprehensive Guide

- Medicare, Medicaid, and Home Care

- In Ontario, Canada, see Local Health Integration Networks (LHIN)

2. Medicare Advantage Enhanced Benefits

When this applies: Medicare Advantage plans (Part C) may offer supplemental home care benefits not available through Original Medicare.

While Original Medicare provides limited home care coverage, many Medicare Advantage plans have expanded their benefits to include services that support aging in place. These benefits change annually, so staying informed about your plan's offerings is crucial.

Enhanced benefits often include:

- Limited personal care services

- Transportation to appointments

- Meal delivery programs

- Home safety assessments

- Additional home health care services

Strategic considerations:

- Benefits change annually - review your plan

- Usually requires prior authorization

- Works well to supplement other funding sources

- Medicare Advantage coordination with other insurance

Learn more about Medicare Advantage Plans at Mediare.gov

3. VA Aid & Attendance Benefits

VA benefits for home care can provide substantial monthly support for qualified veterans and survivors. The veterans home care program offers Aid & Attendance benefits for those who need assistance with Activities of Daily Living (ADLs).

Who is eligible for the veterans home care program?

- Wartime veterans requiring daily assistance

- Surviving spouses of qualified veterans

- Those meeting financial and medical criteria

VA home care assistance amounts (2025):

- Single veteran: Up to $1,794 per month

- Veteran with spouse: Up to $2,050 per month

- Surviving spouse: Up to $1,153 per month

How to apply for VA home care benefits: Applications take 6-12 months to process, but benefits are retroactive to the application date.

Read more:

- Veterans Pensions Can Help Pay for Home Care for Your Loved One

- Veteran Care Services: In-Home Care for Veterans

4. VA Community Care Program

When this applies: Veterans who cannot receive needed care at VA medical facilities may qualify for VA community care services, including home health care through community providers.

The VA Community Care program expands access beyond traditional VA facilities, allowing eligible veterans to receive home care services from community providers when VA care isn't readily accessible.

VA Community Care for home health care includes:

- Home health care services through approved community providers

- Coverage when VA facilities cannot provide needed care

- Geographic accessibility considerations

- Coordination with existing VA benefits

Veteran home care services eligibility:

- Live more than 40 minutes from VA facility

- Cannot get needed care within 30 days at VA

- Specific medical conditions requiring home care

- Prior authorization through VA

Strategic considerations:

- Must receive prior approval from VA

- Can coordinate with VA Aid & Attendance benefits

- Use approved community providers

- Maintain VA enrollment and eligibility

Learn more about the Community Care program at VA.gov

5. Private Home Care Insurance and Long-Term Care Policies

When this applies: Insurance for in-home care services can provide comprehensive coverage when purchased before needing care. Does this insurance cover home health care completely? It depends on your specific policy and the type of services needed.

Long-term care insurance benefits:

- Daily benefit amounts are typically $100-500+

- Coverage for multiple care settings, including home

- In-home health care insurance coordination

Does private insurance cover home health care? To provide coverage, most policies require the inability to perform 2-3 Activities of Daily Living (ADLs).

Read More:

- The Cost of Long-Term Care

- Long-Term Care Insurance

- ADLs and IADLs: The Foundation of Personalized In-Home Care for Seniors

6. Auto Insurance Coverage for Care Needs

When this applies: Auto insurance may cover home health care services following vehicle accident injuries during recovery and rehabilitation periods.

Many people don't realize that auto insurance policies often include medical payment coverage and personal injury protection (PIP) that can fund in-home care during accident recovery. This coverage bridges the gap between hospital discharge and full recovery.

Auto insurance benefits for home care typically include:

- Medical payments coverage for accident-related injuries

- Personal injury protection (PIP) in no-fault states

- Home health care services during the recovery period

- Coverage periods vary by policy limits

Strategic considerations:

- Review your policy before needing care

- Understand coverage limits and time restrictions

- Coordinate with other insurance sources

- Keep detailed records of accident-related care needs

7. Workers’ Compensation Coverage

When this applies: Work-related injuries requiring home health care during recovery may be covered through workers’ compensation insurance.

Workers’ compensation extends beyond initial medical treatment to include home care services during recovery from workplace injuries. This coverage ensures injured workers receive necessary care while transitioning back to independence.

Workers’ compensation benefits for home care:

- Medical care coverage for work injuries

- Personal care assistance during recovery

- Home health care services coordination

- Disability benefits to help cover care costs

Strategic considerations:

- Report workplace injuries promptly

- Use approved healthcare providers

- Coordinate with case managers

- Understand the duration of coverage benefits

8. Life Insurance Policies as Care Funding

When this applies: Life insurance policies with cash value or accelerated death benefits can fund home health care costs through policy loans or benefit acceleration.

Many permanent life insurance policies build cash value that can be accessed for home care expenses. Additionally, accelerated death benefit riders allow early access to policy benefits when facing qualifying health conditions.

Life insurance funding options include:

- Policy loans against cash value

- Accelerated death benefits for terminal/chronic conditions

- Life settlements for older policies

- Viatical settlements for terminal illnesses

Strategic considerations:

- Review existing policies for available benefits

- Understand the impact on death benefits

- Consider the tax implications of policy loans

- Evaluate settlement options carefully

9. Reverse Mortgage Funding Strategy

When this applies: Homeowners aged 62+ can use reverse mortgage proceeds to fund home care costs while remaining in their homes.

A reverse mortgage allows homeowners to convert home equity into cash, specifically for paying for home care expenses. This strategy helps people afford care while staying in familiar surroundings.

Reverse mortgage benefits for home care:

- Monthly payments or a lump sum for care expenses

- No monthly mortgage payments required

- Remain in your home while receiving care

- Funds can cover any home care fees

Strategic considerations:

- Must be the primary residence and meet age requirements

- Consider the impact on inheritance and family finances

- Compare with other home equity options

- Work with HUD-approved counselors

10. Back-Up Care Benefits

When this applies: Emergency dependent care through employer benefits can be used when regular care arrangements fall through unexpectedly or during a family caregiver's illness.

Many employers offer back-up care benefits as part of their employee assistance programs. While not designed for long-term home care, these benefits provide crucial bridge support during care transitions or emergencies.

Back-up care typically covers:

- Emergency care when the regular caregiver is unavailable

- Short-term support during family caregiver illness

- Coverage periods ranging from days to several weeks

- In-home care coordination through employer networks

Strategic considerations:

- Register before you need benefits

- Understand annual usage limits and co-payments

- Use as bridge funding during care transitions

- Coordinate with long-term funding sources

11. Behavioral Health Services Integration

When this applies: Mental health conditions requiring in-home care support may qualify for specialized behavioral health funding through various insurance and state programs.

Behavioral health coverage increasingly recognizes that home care can be more effective than institutional settings for many mental health conditions. This funding source applies particularly to individuals living with depression, anxiety, PTSD, and other conditions requiring daily living support.

Behavioral health funding for home care includes:

- Mental health parity coverage through insurance

- State behavioral health programs

- Specialized home care services for mental health needs

- Integrated care coordination

Strategic considerations:

- Verify mental health parity coverage in your insurance

- Work with providers experienced in behavioral health

- Coordinate with mental health professionals

- Understand documentation requirements for coverage

12. Intellectual & Developmental Disabilities Funding

When this applies: Individuals living with intellectual and developmental disabilities often qualify for state waiver programs that fund home care services as an alternative to group home or out-of-home care.

State Medicaid waiver programs prioritize home care for people living with intellectual and developmental disabilities, recognizing that home-based care costs significantly less than out-of-home placement while providing better quality of life.

Home care funding for developmental disabilities includes:

- Medicaid Home and Community-Based Services (HCBS) waivers

- State developmental disabilities agencies

- Personal care and companion services

- Respite care for family caregivers

Strategic considerations:

- Contact your state's developmental disabilities agency

- Understand waiting lists for waiver programs

- Explore emergency funding for crisis situations

- Consider family support programs

Read More:

13. Private Pay for Home Care

How much does private home care cost per hour? Private home care rates vary by location and level of service but offer maximum flexibility and immediate access to care.

Private pay funding strategies:

- Personal savings and retirement accounts, including Social Security payments

- Family contribution plans among siblings

- Home equity options (reverse mortgages, downsizing)

- Asset liquidation when appropriate

Read more:

14. Other Options, Like Community and Government Assistance Programs

When this applies: Various state, local, and nonprofit programs offer grants and assistance specifically for elderly care at home and other specialized populations who need help with home care costs.

Beyond major funding sources, numerous home care grant programs exist at the federal, state, and local levels. These programs often focus on specific populations, emergency situations, or income-qualified families needing home care support.

Home care financial assistance includes:

- Area Agencies on Aging emergency funds

- State senior services programs

- Medicaid Home and Community-Based Services (HCBS) waivers

- Local community foundation grants

- Faith-based organization assistance

- Condition-specific organizations (Alzheimer's Association, American Cancer Society)

- Home care grant program opportunities through nonprofits

- Employer benefits (FSA, HSA, EAP programs)

Strategic considerations:

- Contact your Area Agency on Aging for comprehensive local resources

- Research state-specific senior assistance programs

- Apply early as funds are often limited

- Each program has specific eligibility requirements

- Best used in combination with primary funding sources

- Combine with other funding sources for maximum benefit

Read more:

Section 3: Creating Your Strategic Funding Plan

Successful Combination Strategies

Most families find success by combining multiple funding sources rather than relying on a single home care payment method.

Example 1: Veteran + Private Pay

- VA home care assistance: $1,794/month

- Private pay supplement: $800/month

- Total budget: $2,594/month

Example 2: Insurance + Family Coordination

- Long-term care insurance: $4,500/month

- Family contributions: $1,000/month

- Total budget: $5,500/month

On a Timeline: How to Pay for Home Health Care

Determining how to pay for home care services successfully requires understanding that different sources have different timelines. It will take time to receive certain types of funding and assistance. Your strategy should cover the following:

Immediate needs (0-30 days):

- Start with private pay while pursuing other sources

- Coordinate family resources for short-term support

Short-term planning (3-6 months):

- Submit Veteran Affairs home care program applications immediately

- Verify Medicare home health care coverage and elimination periods

- Research community programs

Long-term planning (1+ years ahead):

- Consider long-term home care insurance if you or your family member is healthy and eligible

- Maximize HSA/FSA contributions

- Create family care agreements

Tax Considerations

Are home health care expenses tax deductible? Yes, many home care expenses qualify as medical deductions. Consult a tax professional for specific guidance.

Read more:

Section 4: Working with Care Providers

When vetting professional providers, ask these questions:

- Which payment sources do you accept and support?

- How do you handle insurance for home care billing and documentation?

- Can you provide transparent cost estimates?

- Do you offer payment plans or sliding-scale options?

Build your care team carefully. Successfully paying for home care often requires coordination among multiple professionals who understand both care needs and financial options.

Section 5: Taking Action – Your Next Steps

Immediate Actions (This Week)

- Download our Home Care Payment Planning Worksheet.

- Contact your local Homewatch CareGivers for area-specific costs.

- Gather important documents and compile a list of current resources.

- Identify the most promising funding sources.

Short-term Planning (30 Days)

- Verify existing benefits and begin applications.

- Research local community resources.

- Schedule professional consultations if needed.

- Have family discussions about care and finances.

Long-term Strategy (90 Days)

- Develop a comprehensive funding plan.

- Establish relationships with qualified providers.

- Create backup plans for changing circumstances.

- Set up tracking systems for expenses and benefits.

Section 6: Frequently Asked Questions about Paying for In-Home Care

What if I need care immediately but haven't planned financially?

Start with private pay for essential services while applying for other sources. Many families begin with limited hours and adjust as benefits become available.

Can I combine multiple payment sources?

Yes, most families use combinations. We help coordinate billing across multiple sources to maximize benefits.

How do I know which funding sources I qualify for?

Use our eligibility screeners and contact your local office for personalized assessment and application assistance.

What can I expect when comparing nursing home care vs. in-home senior care cost?

The cost of home health care for seniors is often more affordable than nursing home placement, with more funding options available.

How much does the VA pay for in-home care?

Depending on eligibility, the Veterans Administration Aid & Attendance Pension benefit may provide up to $1,794 per month for a veteran’s home care needs. Veterans’ spouses and survivors may also qualify for home care benefits.

What's the average cost of a caregiver?

The cost of services is different for each client based on many factors. Learn more about the average cost of home care in specific areas by visiting this resource.

Does Social Security pay for in-home care?

Neither Supplemental Security Income (SSI) nor Social Security Disability Insurance (SSDI) will pay for home care services directly. However, Social Security benefits can be used to pay a home care provider.